يحاول ذهب - حر

PRIORITY SECTOR LENDING CERTIFICATES (PSLC)

April 2023

|BANKING FINANCE

Priority Sector Lending Certificates is a tool for promoting comparative advantages among banks while they meet their priority sector lending obligations in India

Introduction:

"Banks with a comparative advantage in lending to the priority sector should earn priority sector lending certificates [social credits] while those falling short of the target would be required to buy priority sector lending certificates [social credits]. A forward market for Priority Sector Lending Certificates [social credits] will help banks to focus and plan well.

Total credit extended by banks in priority sector lending was INR 21,543,562.9 million (US$322,361 million as of June 2016) towards the end of financial year 2015. The goal of Priority Sector Lending Certificates is to create market efficiency in priority sector lending "to increase employment, create basic infrastructure and improve competitiveness of the economy, thus creating more jobs. Priority Sector Lending Certificates is a method for directing credit and could be used in Asia and other parts of the world as an alternative method for directing credit.

Background:

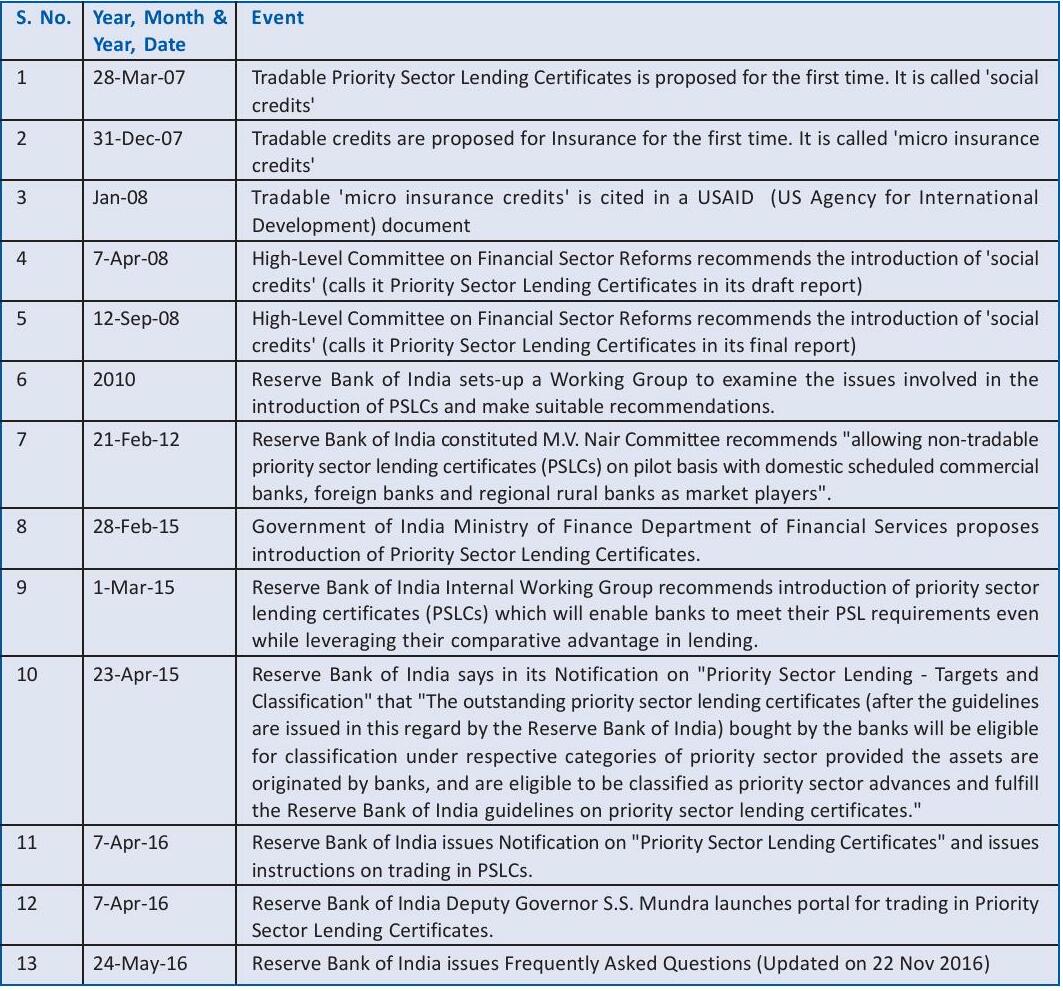

Tradable Priority Sector Lending Certificates was first proposed by Mr. A. M. Godbole in his article "How to lend more to the poor" (Mint, 28 March 2007). Mr. A. M. Godbole had called tradable Priority Sector Lending Certificates as 'social credits'. On 7 April 2008 (in a draft report) and on 12 September 2008 (in a final report) the High-Level Committee on Financial Sector Reforms recommended the introduction of Priority Sector Lending Certificates. On 7 April 2016 the portal for trading Priority Sector Lending Certificates was launched by the Reserve Bank of India. Within twelve months of the launch of the Priority Sector Lending Certificates portal for trading, a total of INR 430.1 billion (US$6.63 billion as of 31 March 2017) of PSLC SF/MF and PSLC General by volume was traded.

هذه القصة من طبعة April 2023 من BANKING FINANCE.

اشترك في Magzter GOLD للوصول إلى آلاف القصص المتميزة المنسقة، وأكثر من 9000 مجلة وصحيفة.

هل أنت مشترك بالفعل؟ تسجيل الدخول

المزيد من القصص من BANKING FINANCE

BANKING FINANCE

The Race for the Super App: Will India's BFSI Ecosystem Converge?

The concept of a Super App has its roots primarily in Asia. The term is often credited to refer to platforms that began with one core function (messaging, ride-hailing, payments) and then expanded to offer a portfolio of services accessed through the same interface. For example, WeChat in China began as a messaging app and evolved into payments, e-commerce, ride-hailing, mini-programs and more.

11 mins

January 2026

BANKING FINANCE

Digital Sustainability

ESG initiatives are vital for organizations aiming to achieve long-term sustainability, resilience, and stakeholder trust. They help businesses address pressing environmental challenges, such as carbon emissions, resource scarcity, and climate change, while ensuring ethical governance and social inclusion.

11 mins

January 2026

BANKING FINANCE

Ravi Ranjan appointed SBI managing director, to oversee risk and stressed assets

State Bank of India (SBI) has appointed Ravi Ranjan as its Managing Director with effect from December 15, 2025, according to a regulatory filing by the country's largest public sector lender.

1 min

January 2026

BANKING FINANCE

Reserve Bank News

Reserve Bank of India has appointed Usha Janakiraman as Executive Director with effect from December 1, 2025, according to an official release issued by the central bank. Her appointment comes just days ahead of the Monetary Policy Committee (MPC) meeting scheduled for December 3.

7 mins

January 2026

BANKING FINANCE

Mutual Fund News

Children's mutual funds, once a niche investment option, are increasingly becoming a mainstream tool for long-term financial planning in Indian households, especially for education-related goals.

7 mins

January 2026

BANKING FINANCE

Co-Operative Bank News

As per the Reserve Bank of India's Report on Trend and Progress of Banking in India 2024-25, State Cooperative Banks (StCBs) and District Central Cooperative Banks (DCCBs), which together constitute the short-term rural cooperative credit structure, reported steady balance sheet expansion, sustained growth in deposits and advances, and improving asset quality during 2024-25.

2 mins

January 2026

BANKING FINANCE

Legal News

Foreign firms can't claim full deduction for head of- fice expenses on Indian biz: SC

5 mins

January 2026

BANKING FINANCE

Banks unlikely to cut deposit and MCLR rates despite RBI repo rate reduction

Despite the Reserve Bank of India delivering a 25 basis points cut in the repo rate last week, banks are unlikely to reduce term deposit rates or marginal cost of funds-based lending rates (MCLR) aggressively, according to senior bankers.

1 min

January 2026

BANKING FINANCE

Government to divest up to 3% stake in Indian Overseas Bank via OFS

Shares of Indian Overseas Bank (IOB) came under selling pressure after the Government of India announced plans to divest up to 3% of its equity through an Offer for Sale (OFS).

1 min

January 2026

BANKING FINANCE

Unclaimed bank deposits in India more than double in five years

India's unclaimed bank deposits have more than doubled over the past five years, rising to Rs. 67,004 crore as on June 30, 2025, from Rs. 27,824 crore at the end of FY21, highlighting a growing challenge for the banking system.

1 min

January 2026

Translate

Change font size